This post stems from research I conducted on the M^0 protocol last year while developing the USDN parking feature for Noble. Beyond Noble in the Cosmos ecosystem, major players like MetaMask and HyperLiquid are already participating as "Earners," issuing and circulating stablecoins based on the $M token.

I believe this protocol features one of the most progressive and decentralized monetary mechanisms among existing stablecoins, and I would like to further develop and share those insights here.

1. Why M^0?

Traditional stablecoins like USDC and USDT are structured such that the issuer monopolizes the yield from collateral (such as interest from U.S. Treasuries). M^0 dismantles this monopoly. It is a decentralized middleware designed to allow qualified institutions to directly mint stablecoins ($M) and share the resulting revenue with ecosystem participants.

Overview

- Collateral Base: Backed by Short-term U.S. Treasury Bills with maturities of 90 days or less.

- Core Actors: Operates a digital dollar called

$M(ERC20 token) through the interaction between Minters, Validators, and Earners. - Smart Contract-Based Transparency:

- Operates on immutable smart contracts on the EVM, ensuring transparency as the protocol code cannot be altered.

- On-chain governance (Two-Token Governor) manages the selection of Minters and Earners.

- Institutional-Grade Infrastructure:

- Guaranteed compliance and legal stability. Only approved institutions (Minters) that comply with real-world financial regulations can participate in minting, with explicit legal redemption rights.

- Adheres to institutional asset protection standards by depositing collateral with independent third-party custodians.

2. The Three Pillars: Actors of M^0

The M^0 ecosystem functions through an organic structure where issuance, validation, and distribution are decoupled.

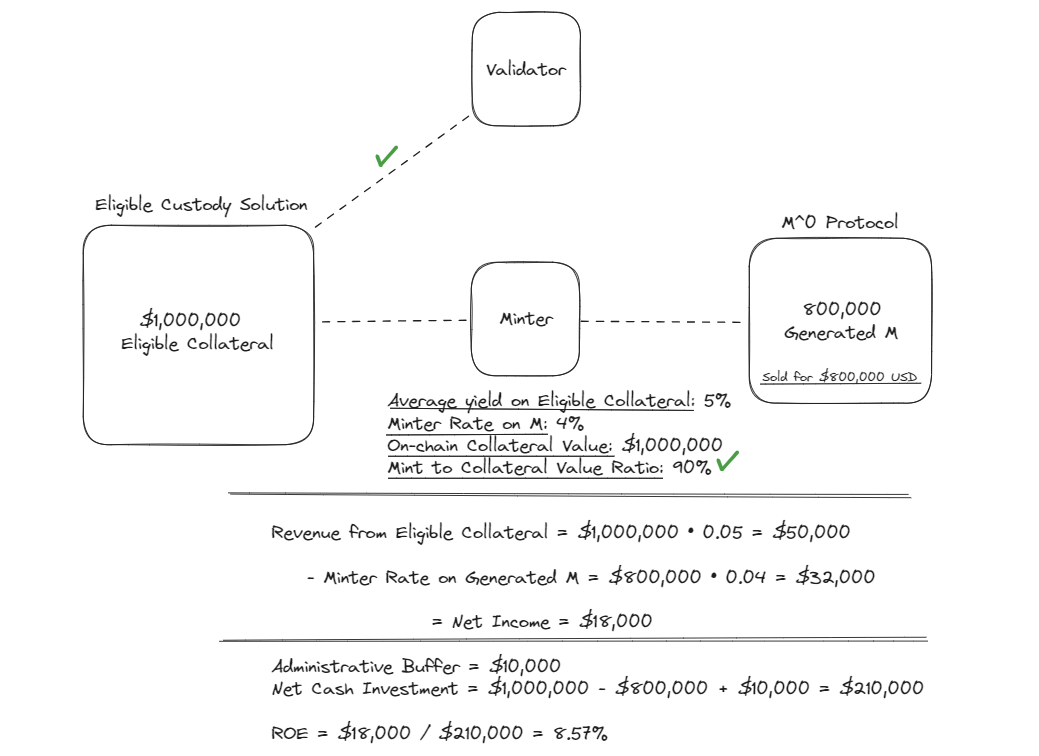

1. Minters (Issuers)

These are approved institutions that comply with financial regulations and mint $M backed by U.S. Treasuries. The first Minter, MXON, began issuance in July 2024.

Role

Minters deposit Treasuries with a separate custodian and mint $M against that collateral.

Fees Paid by Minters

- Minter Rate: A fee charged every time $M$ is minted. This rate is distributed to Earners and

$ZEROtoken holders to promote protocol stability and participation. - Penalty Rate: A punitive fee imposed if a Minter fails to comply with protocol regulations.

Revenue Structure

- The spread between the interest generated by the deposited Treasuries and the Minter Rate paid to the protocol.

- Sales of

$M.

Over-collateralization

Minters must maintain an over-collateralized state. If the collateral value drops, they must deposit additional assets or burn $M$. Violations trigger penalties and automated collateral liquidation.

Revenue structure: Spread between Treasury interest and Minter Rate + $M sales

2. Validators

Validators ensure the protocol's integrity, but their nature differs from typical PoS validators.

Role

- Real-time Collateral Verification: They verify the validity of off-chain collateral held by Minters, generate digital signatures, and approve on-chain minting.

- They act as "watchdogs" through off-chain incentives or governance contracts to prevent fraudulent minting.

Reward System

While on-chain direct rewards are minimal, Validators can earn incentives through the liquidation of non-compliant Minters' collateral or via reward structures set by governance.

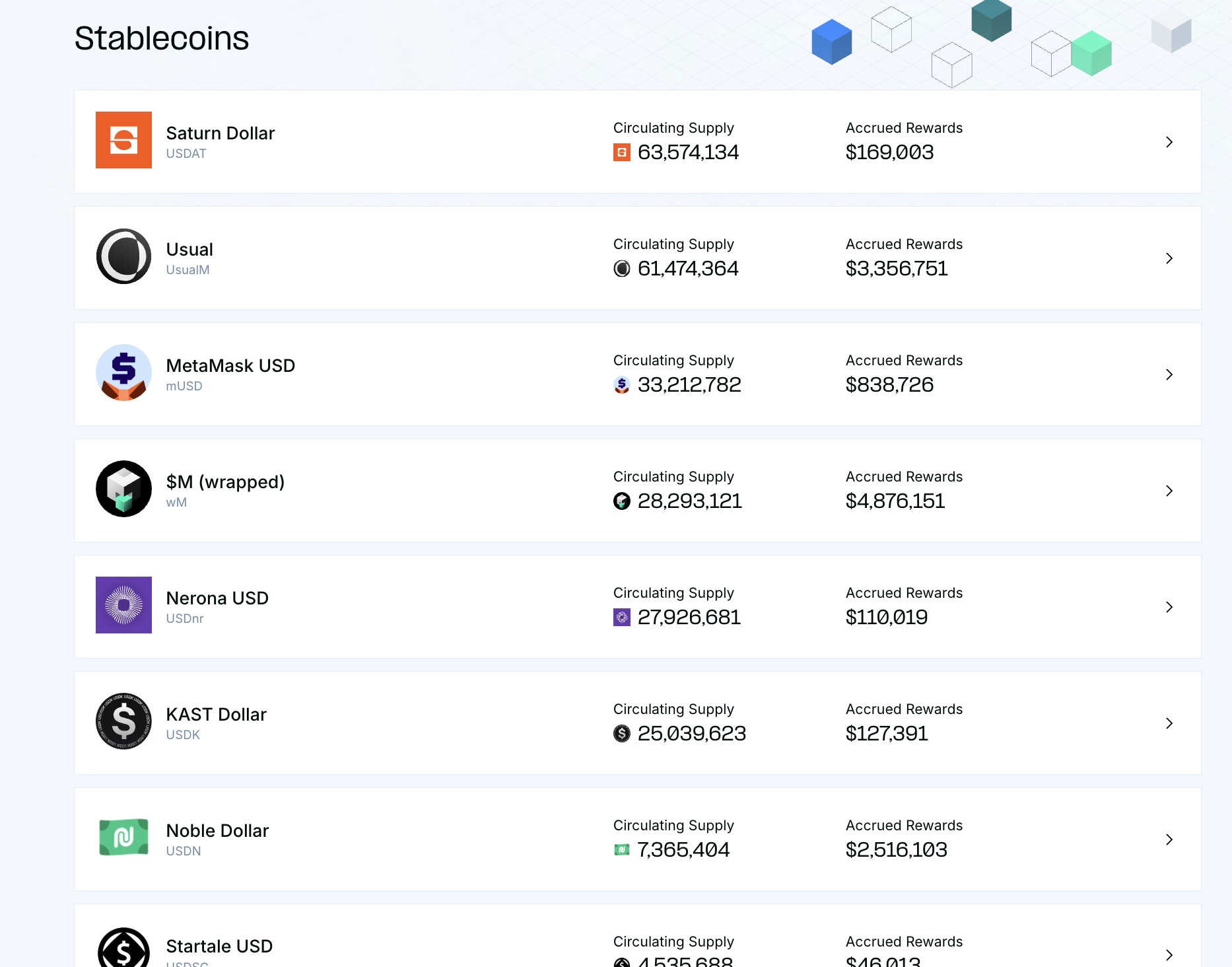

3. Earners (Beneficiaries/Distributors)

These actors hold $M and provide liquidity to drive protocol growth (e.g., Noble, major exchanges, and DeFi protocols).

Role

Earners purchase $M from Minters to supply it to the market or stake it in the "Earn Mechanism" to generate yield.

Reward System

- Earner Rate: The interest rate paid to Earners holding $M$, determined by the TTG (The Top Governor). It is expected to stay near the U.S. Federal Funds Rate to incentivize continuous holding. This rate can be adjusted to manage $M$'s peg to $1.

- Minter Fees: A portion of the fees generated during the minting and redemption of

$M. As network liquidity increases, the value added for Earners grows. - Yield Distribution: Sharing of profits generated from the underlying collateral backing

$M.

Current supply and reward status of active Earners

2.5. The Foundation of Trust: Off-chain Ecosystem

M^0 distinguishes itself from simple algorithmic stablecoins through its robust integration with real-world financial systems and legal frameworks.

- Minters as Legal Entities: Minters are not just wallet addresses; they are approved institutions that bear legal liability for collateral assets in the physical world.

- Independent Custody: Instead of Minters holding assets themselves, Treasuries are deposited with independent third-party custodians approved by governance, providing dual-layer security.

- Real-time Oracle Verification: Using oracle solutions like Chronicle, the protocol monitors the status of off-chain collateral in real-time and synchronizes it with on-chain data, enabling "transparent on-chain verification."

- Legal Redemption Rights:

$Mholders are protected by a design that grants them legal rights to the underlying collateral, ensuring the digital asset corresponds 1:1 with real-world value.

3. Governance: Two-Token Governor (TTG)

M^0 employs a unique on-chain governance system using two tokens to prevent the concentration of power.

Token Types

$POWER: Voting Power (Active Governance)- Used for functional voting, such as selecting Minters/Earners and setting key interest rates.

- Holders must actively participate in voting to maintain their influence.

$ZERO: Governance Token (Passive Governance)- $ZERO holders lock (stake) their tokens to acquire $POWER for active voting.

- They serve as the "last line of defense," holding the power to reset or veto harmful decisions made by $POWER holders, thereby ensuring the fundamental stability of the TTG system.

- A portion of protocol revenue (Minter Rates, etc.) may be attributed to $ZERO holders.

Governance Responsibilities

- Key Parameter Management:

- Mint Ratio: The ratio of collateral value that can be converted into

$M. - Minter Rate: The fee percentage paid by Minters when issuing

$M. - Earner Rate: The interest rate paid to Earners holding

$M.

- Mint Ratio: The ratio of collateral value that can be converted into

- Participant Management:

- Actor Management: Approving and managing the qualifications and authority of key institutions like Minters.

- Custody Management: Selecting custodians and setting asset protection protocols.

Operational Cycle

The TTG operates in 30-day Epochs, divided into two distinct 15-day phases.

Phase 1: Transfer Period (Day 1–15)

The preparation phase of the epoch.

- Power Transfer: $POWER holders prepare to exercise their voting rights.

- Proposal Discussion: The community and stakeholders informally discuss and coordinate on proposals for the next phase.

- Staking Activation: Holders wishing to vote must finalize their voting power during this window.

Phase 2: Vote Period (Day 16–30)

The decision and execution phase.

- Voting: Participants with finalized voting power cast their votes on on-chain proposals.

- Parameter Finalization: Specific values for protocol settings are determined.

- Execution: Protocol settings are updated based on the vote, taking effect immediately or in the following epoch.

This cycle allows the protocol to respond continuously to market conditions (e.g., changes in the Fed Funds Rate). The 15-day voting window prevents market chaos from sudden changes and ensures deliberate decision-making.

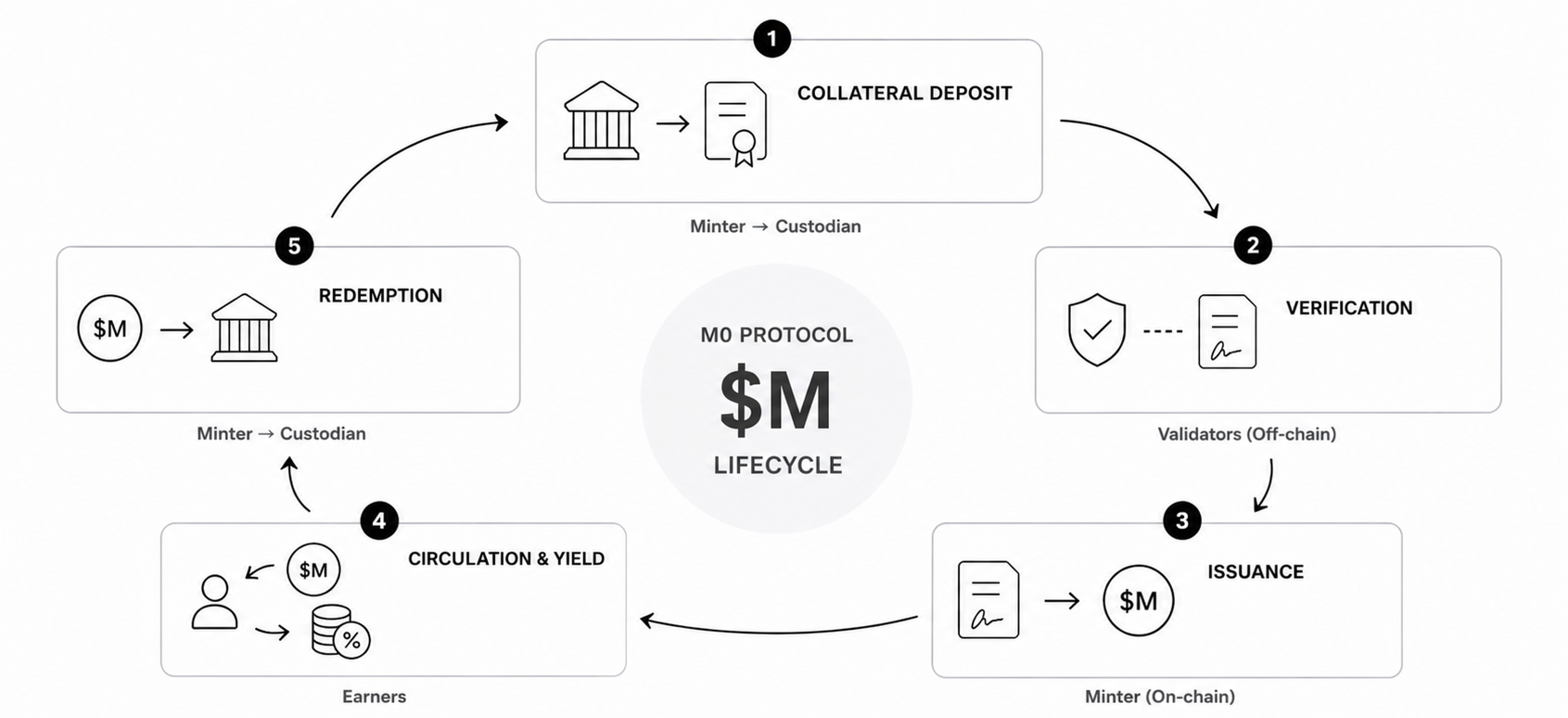

4. Cycle of $M

- Collateral Deposit: A Minter deposits U.S. T-Bills with an eligible custodian.

- Verification: A Validator verifies the off-chain collateral and issues a minting signature.

- Issuance: The Minter mints

$Mon-chain to secure liquidity. - Distribution & Interest: An Earner purchases/stakes

$Mand receives a portion of the Treasury-based yield. - Redemption: The Minter burns

$Mand retrieves the deposited Treasuries.

5. $M vs. Traditional Stablecoins

$M differentiates itself through transparency and yield sharing.

| Feature | USDT (Tether) | USDC (Circle) | M^0 ($M) |

|---|---|---|---|

| Issuer | Single Issuer (Tether Ltd.) | Single Consortium (Centre) | Multiple Approved Institutions (Minters) |

| Collateral | Mixed (Cash, T-Bills, Loans, etc.) | Cash & T-Bills | 100% U.S. T-Bills |

| Transparency | Opaque (Attestation reports) | Relatively Transparent (Regular audits) | Real-time On-chain Verification |

| Yield Sharing | Issuer monopolizes interest | Issuer monopolizes interest | Shared with Holders (Earners) |

| Risk | Qualitative risk of assets | Centralization & Banking risk | On-chain collateral valid even if institutions fail |

6. Conclusion and Outlook

The M^0 protocol is more than just a stablecoin; it is an infrastructure for the "on-chaining of Treasuries."

$M disrupts the monopolistic revenue models of specific issuers and creates a powerful network effect by redistributing yield to the Earners who drive distribution. While Tether and Circle represent centralized revenue models, M^0 is a symbiotic middleware where all participants share the rewards.

Ultimately, a structure where institutions directly mint and generate revenue, while distributors share in the fruits of that labor, will be the driving force for $M to become the standard digital dollar in the burgeoning RWA market.